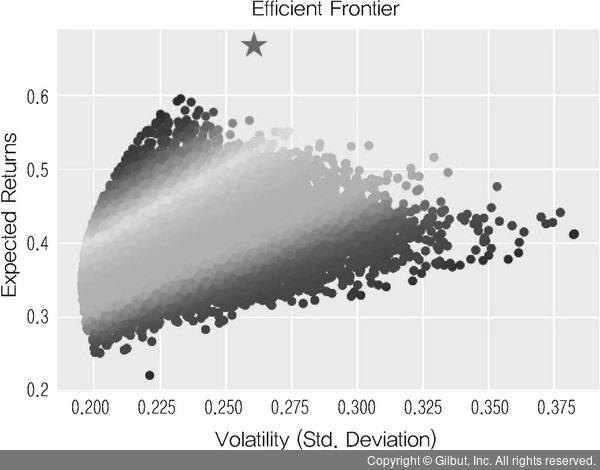

다음은 최적화 결과를 차트로 그리기 위한 코드다. 코드는 n개의 종목으로 다양한 투자 비중을 조합해 구성한 30,000개의 포트폴리오를 만든다. 투자 비중은 랜덤하게 정해지며, 그 합계는 1.0(100%)이다. 또한, 수익률, 위험을 계산하고 수익률, 위험, 투자 비중을 리스트에 담는다.

그리고 matplotlib를 이용해 여러 가지 효과를 준 분산형 차트로 그린 것이다.

p_returns = [ ]

p_volatility = [ ]

p_weights = [ ]

n_assets = len( tickers )

n_ports = 30000

for s in range( n_ports ):

wgt = np.random.random( n_assets )

wgt /= np.sum( wgt )

ret = np.dot( wgt, ret_annual )

vol = np.sqrt( np.dot( wgt.T, np.dot(cov_annual, wgt ) ) )

p_returns.append( ret )

p_volatility.append( vol )

p_weights.append( wgt )

rets = np.sum( ret_daily.mean( ) * res[ 'x' ] ) * 250

vol = np.sqrt( res[ 'x' ].T @ covmat @ res[ 'x' ] )

p_volatility = np.array( p_volatility )

p_returns = np.array( p_returns )

colors = p_returns/p_volatility

plt.style.use( 'seaborn' )

plt.scatter( p_volatility, p_returns, c=colors, marker='o', cmap=mpl.cm.jet )

plt.scatter( vol, rets, marker="*", s=500, alpha=1.0 )

plt.xlabel( 'Volatility (Std. Deviation)' )

plt.ylabel( 'Expected Returns' )

plt.title( 'Efficient Frontier' )

plt.show( )

결과

▲ 그림 4-21 샤프비율 최적화 결과